Now in its 85th year, the annual Prospectors & Developers Association of Canada's Convention, or PDAC, is the world's leading mineral exploration and mining event. PDAC attracts investors, analysts, mining executives, prospectors, geologists, government officials and students. The convention is open to the general public and the majority of events are free, making this an attractive event for those interested in investing in the sector and doing their own due diligence. Some event highlights include:

- Presentations for Investors: Newsletter writers/analysts present their charts, thoughts and ideas on how to select good investments in the resource sector.

- Prospectors Tent: Self-employed/independent prospectors display their results and samples.

- Trade Show: Organizations and governments promote the latest technology, products, services and mining jurisdictions.

5i Research attended the event to get a ground floor perspective with a focus on general sentiment towards the sector and how some of the smaller miners pitch their company to investors.

![]()

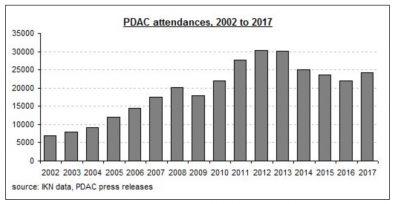

Attendance at PDAC 2017 totaled 24,161. As per PDAC communications, this figure exceeded expectations and was a strong indication that confidence has returned to the mineral exploration and mining industry. The industry is of course cyclical in nature and has faced a variety of economic challenges over the past several years. Indeed, having attended the event last year, the sentiment was night and day. Last year, events were relatively poorly attended and it was hard to find an upbeat vibe throughout the convention. This year, investors were certainly more enthused. Attendance was two thousand more than last year and slightly up on 2015 but was lower than 2014 and from the 30,000+ peaks of 2012 and 2013.

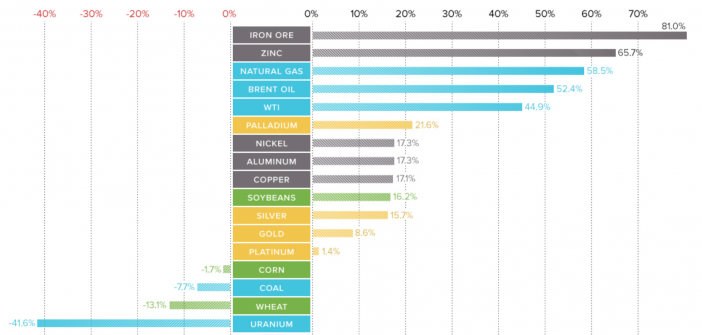

Base metal prices had an excellent 2016 and this is certainly responsible for driving much of the miner optimism and investor enthusiasm. In particular, investors were most interested in how to get more exposure to zinc in their portfolios. It’s not hard to see why someone might look to benefit from recent momentum in zinc or iron ore prices. Below we show base metal performance over 2016:

source: http://www.visualcapitalist.com/chart-every-commodity-2016/

Getting in on the Action

With this, we were interested in attending the Trevali Mining Corporation (TSX.V: TV) presentation and it was one of our favourite of the day. The stock is up 210.0% over the last year and trades at a $475-million market-cap. This is a zinc-focused, base metals mining company with two commercially producing operations. The company is actively producing zinc and lead-silver concentrates from its 2,000-tonne-per-day Santander mine in Peru and its 3,000-tonne-per-day Caribou mine in New Brunswick.

TV is the primary zinc producer on the TSX. Fundamentals for the base metal continue to appear bullish with recent global production closures, global concentrate deficits and continued strong demand. Needless to say, with a high flying stock the presentation was well attended and the presenter had to do little to sell the company thesis. Further strengthening the company’s appeal is that there is “zinc production now to benefit from rising zinc prices now”. Unfortunately for miners looking to get into the space there are not a lot of viable zinc projects because it has been such an underinvested space globally for many years.

The company also has a strategic partnership with Glencore, one of the world’s largest zinc miners and commodity traders. This partnership has allowed TV to leverage the expertise and technology of Glencore, and ultimately helped the zinc miner de-risk some of its operations.

Most investors with their finger on the pulse of the mining sector are looking for zinc. TV looks to be in a good position with producing assets that can take advantage of zinc price momentum ‘today’ should the cycle persist. Of course, a change in price could change the return profile on this stock quickly.

Another interesting presentation with a zinc tilt was Altius Minerals Corp (ALS). Altius is a diversified mining royalty company with royalty and royalty-like interests in 14 producing mines located in Canada and Brazil. The interests include mining operations that produce copper, zinc, nickel, cobalt, gold, silver, potash, thermal (electrical) and metallurgical coal. ALS is interesting as most industry royalty names are focused in gold (or precious metals). ALS is a diversified mining royalty vs. just holding a portfolio of one or two commodities. In our opinion, the diversified royalty business is a smaller market and this may give ALS an advantage.

Although markets value ALS as a royalty business, they consider themselves more so as a project generation business, and this is where the company’s current assets are rooted. The company has a history of being a contrarian buyer, holding the property until the market turns, selling the asset to a junior, taking an equity stake and then generating royalties from the sale.

If you believe copper and zinc are going higher, ALS certainly has some upside to these metals, which should result in a higher cash flow (and stock price). However, we will note that we found this to be one of the ‘salesy’ presentations of the day. While forward looking statements are common at investor day presentations (and were disclosed by ALS), we found some of the statements made here to be aggressive, as they implied a higher degree of certainty around future results. Some of these comments are mentioned in closing.

What’s Better than Cash? More Cash

Another interesting presentation was Sandstorm Gold Ltd. (TSX: SSL), a gold streaming and royalty company. The stock was up 135.0% over the 2016 gold run but over the last year has come off and shows a return of 36.0% over this period. SSL trades at a $475-million market-cap.

Sandstorm provides upfront financing to gold mining companies that are looking for capital and in return, receives the right to a percentage of the gold produced from a mine, for the life of the mine. Sandstorm has acquired a portfolio of 142 streams and royalties, of which 21 of the underlying mines are producing gold. A stream allows Sandstorm to purchase a portion of a mine’s gold production at a fixed price per ounce. With a gold royalty, Sandstorm receives a portion of the revenue generated from a mine's operations.

Much of the presentation and Q&A surrounded the ‘optionality’ Sandstorm had to gold prices, or put another way, the high degree of cash flow growth that would result from an increase in gold prices. For example, based solely on the producing assets today, the company expects to generate cash flow of $60-million in 2021 (generated $30-million in 2016). At $1,600 gold per oz, SSL generates $100-million just through increased production of current assets. However, the production/cash flow profile does not take into account investments that have already been made where the timing of the asset going into production is not known with certainty. Once these assets come online, SSL sees significant upside to its cash flow. Most investors with rising gold prices buy mining companies because of the high degree of leverage in their profile but these operators do not generate much in that of cash flow.

Are Things Are Moving Too Fast?

It is easy to get caught up in the optimism of an excellent year for commodity prices. Indeed, pitches for next year’s success stories were not a rare find (no pun intended). Here are some phrases that stood out from other presentations and booth visits:

- “We are a $500-million market-cap company, but we think we should be a $750-million stock”

- “I know these projects are going to make us 100’s of millions; they are going to be worth a lot more”

- “We sit on $12-million in equity stock and think it’s going to be $100-million very soon”

- “Last year wasn’t our year but just hang on and stay with us”

- “The market simply doesn’t recognize the value of what we have in the ground”

- “We see 180% upside potential on the stock to get us back to our old highs”

Maybe some of the companies are right. Maybe the value of the stock or assets does double. Maybe investors just do not see the potential yet. Unfortunately, investing on these pitches is speculation at best. Forecasting the future of any asset class is difficult; forecasting commodity prices is a whole new ball game. If you feel like you are being ‘sold’ an investment, it is prudent to proceed with caution.

Comments

Login to post a comment.