Through the 5i Research Q&A service, we are frequently asked for our preferred ranking of industry related companies. This article will be a first in a series where we compare and evaluate the prospects behind a group of industry peers that operate within both a similar environment and business model.

In this blog our focus will be on the food retail industry and our focus list of companies (“the group”) we include: Empire Co Ltd. (“Empire”), Metro Inc. (“Metro”) and Loblaw Companies Ltd (“Loblaw”). The blog will highlight major themes and metrics that are drivers of constituent returns. The blog is a summary piece and not intended to be a full company analysis; investors are encouraged to perform their own due diligence.

Investment Summary and Top Pick

Of the group, we would prefer Loblaw at this time for its growth profile behind the Shoppers acquisition, best in-class margins and solid free cash flow generation. Metro is a close second however, and these two names often switch back and forth as analyst favourites.

One can debate that Metro even has more growth potential behind the stock, and valuations reflect this, but Loblaw is tough to beat for that defensive ‘sleep at night’ quality. If you are making an investment in the consumer staples sector, you are likely doing so for a defensive play.

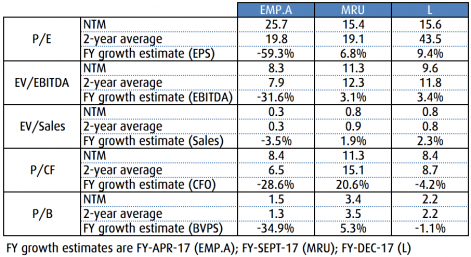

Both Loblaw and Metro are trading at a forward price-to-earnings (P/E) of approximately 15.5x, which is at a discount to historical averages and the TSX. Otherwise, Metro trades at a premium to Loblaw by most valuation metrics.

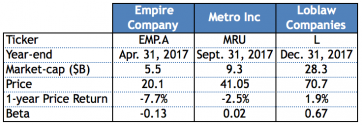

Empire would be a 3rd tier pick and it has been a tough name to hold the last year or so after a poor integration of the Safeway acquisition in Western Canada. The stock hit a low of $14.74 to end 2016, and over that year was down -40.0%. The stock price reflects the Safeway results and there may be significant upside from here for the more aggressive investor who is willing to take a shot at a company turnaround and has a long-term time horizon. Indeed, the stock is up 28.1% year-to-date (YTD) on good Q32017 results.

However, with a new CEO (on January 12, 2017, Michael Medline was named as President and CEO of Empire and Sobeys), do not expect a turnaround to happen over night. We would like to see a couple quarters of good news before getting overly excited about this name.

Its All About Who You Know

It is difficult to increase consumer demand for industry products and services, as consumption remains a constant. So how do sector companies grow their businesses and ultimately their stock prices? Brand recognition will ultimately drive growth in market share and likely trumps other factors from a long-term, sustainable impact perspective.

Under Empire’s umbrella are Sobeys, IGA, Safeway, Foodland or Fresh Co. stores. Empire also generates sales from Pharmacy, Liquor and Fuel sales. In addition to the well-respected Loblaw brand, Loblaw also offers a discount retail brand through its Real Canadian Superstore and Joe Fresh networks, pharmacy products via its Shoppers Drug Mart acquisition, and President’s Choice Financial services. Metro operates both superstore and discount food retail businesses under the Metro and Food Basics brands, as well as local market names like Marche Ami, and Brunet drugstores.

Loblaw has the largest share of the market with $10.8 billion in sales, as of the last reported quarter. This almost doubles Empire, the next in line with $5.9 billion. Over the last four quarters shown, Loblaw has increased retail sales 2.3%. Empire’s retail sales have dropped by the same figure, mostly due to continued negative impacts from its Western Canada expansion strategy (Safeway). Metro is roughly flat. Clearly, revenue momentum is in Loblaw’s favour, and the company is increasing market share vs. the peer group.

We broke out Loblaw’s drug retail segment to show how important the Shoppers Drug Mart acquisition has been for the company. With it, Loblaw has the largest peer group exposure to the drug retail business and this should be a nice source of growth and stability for the company going forward. With an aging Canadian population, it is hard to argue against the demographics and rationale of this business line. Overall, Loblaw did a solid job of integrating the acquisition. The company achieved the synergies they indicated when they bought Shoppers. In addition, Loblaw went through a refurbishment program and put new SAP systems in place. The company is seeing the benefits of these strategies.

For the most recent quarter, Loblaw showed same-store-sale (s-s-s) growth of 3.4% and 1.1% in its drug retail and food retail businesses, respectively. SSS growth for Metro was 0.7% (a significant drop from previous quarters) and -3.1% for Empire. This metric represents the percentage change of sales in the company's stores that have been operating for a year or more. Investors frequently use same-store sales to determine the effectiveness of the management of a retail chain in producing revenue growth from existing assets.

Cheque Please!

In addition to the defensive qualities of these businesses and diversification of equity returns away from the broad market, investors expect industry names to generate consistent cash flows and fund a growing dividend. Unfortunately, the absolute level of the yield likely will disappoint, as investors in a yield-hungry world have bid-up the price of high quality companies that pay a dividend, driving yields lower.

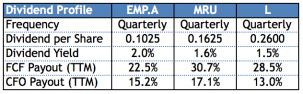

Empire is this highest yielding stock of the group at 2.0% and this could be attractive to a more aggressive dividend equity investor. With a trailing 12-month (TTM) free cash flow payout ratio of 22.5%, this is low enough that the company should have flexibility to do another increase in 2017. Management uses free cash flow as a measure to assess the amount of cash available for debt repayment, dividend payments and other investing or financing activities. We calculate free cash flow as (operating cash flow) – (capital expenditures) – (interest paid).

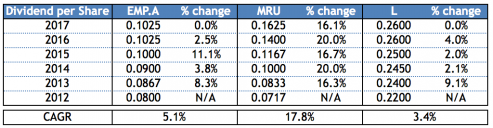

Metro is another standout here and has been the most aggressive in increasing its dividend to shareholders, with a compounded annual growth rate (CAGR) of 17.8%. Considering a CAGR of 5.1% and 3.4% for Empire and Loblaw, this is quite impressive. With that, it does have the highest payout ratio of the group but this is at a level that should not cause on discomfort. Metro aims to pay total annual dividends representing a range of 20% to 30% of the prior fiscal year's net earnings, excluding non-recurring items, with a target of 25%. On an annualized basis, the current dividend represents 25.0% of the target measure.

Marginally Important

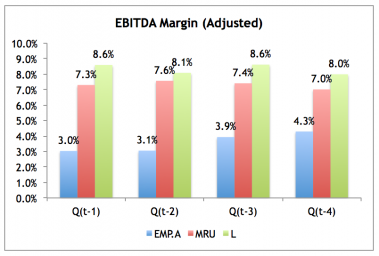

Margins are tight in the industry and any change to the price (or cost per unit) can have a large impact on the bottom line. This also means that prices can only be reduced so much before it becomes unprofitable to do so. Gross and EBITDA margin is an important indicator of cost control and can help management, analysts and investors assess the competitive landscape.

Loblaw and Metro have higher EBITDA margins for the industry, at 8.6% and 7.3%, respectively. Compared to Empire at 3.0%, this means these two companies benefit from increased flexibility to adjust prices to attract price sensitive customers, or have more room to operate in poor industry conditions without threatening the underlying business. For example, industry names could find themselves in a scenario where food costs are inflationary but the business is unable to pass on the added cost to the consumer. Here, having flexibility through higher margins is a comfort.

Valuation and Outlook

By most measures, Metro is the most expensive stock of the group. The stock trades at a lofty EV/EBITDA of 11.3x, a premium of 18.6% to Loblaw, and a P/B of 3.4x. Markets are paying for an expected higher growth rate with metrics like cash flow per share (CFOPS) expected to increase 20.6% on the year. Dividends are of course paid out of cash flows so this could in turn help to fund a higher dividend growth rate. In 2016, the company invested $350 million, opened six stores and carried out major renovations in 43 others. Metro expects to invest a further $350 million in the store network over 2017, mainly for new store openings, expansions and remodels. Metro also has a 5.7% (5.7% in 2015) interest in Alimentation Couche-Tard (ATD.B) a publicly traded associate in the convenience store industry. Alimentation has expanded internationally and has done a great job of growing by acquisition. This should as well provide a nice boost to Metro’s earnings profile and is a nice way to get exposure to another Canadian retail name.

Loblaw looks to continue to steal market share from its peers with expected revenue growth of 2.3%. In our opinion, capturing market share continues to be the most important driver of stock returns over the long-term. Loblaw expects to invest approximately $1,300 million in capital investments in 2017. Approximately 44% of these funds are expected to be dedicated to investing in retail operations, 27% will be spent on IT and supply chain projects, 23% on Choice Properties’ development projects and 6% on infrastructure and other projects.

Valuations on Empire are less useful simply due to the volatility of the underlying fundamentals. The company’s expected growth rates reflect the April 31, 2017 year-end. While 2018 figures are available and likely more useful, we used the more negative short-term results to highlight some of the potential risk to the stock price (up almost 30.0% YTD) when the company reports its 2017 full year. YTD results of fiscal 2017 have reinforced the need for significant expansion and acceleration of efforts to reduce costs throughout the organization. Empire also intends to address the “complex organizational structure, which has resulted in duplication and lack of clearly defined accountabilities.”

In regards to the industry outlook, the price sensitivity of consumers has grabbed investor’s attention. Companies are listening to the consumer and have started to be more competitive on pricing. For example, Empire, Metro and Loblaw have all lowered prices to try to be a little bit more competitive. Here is an example of where higher margins give operators flexibility and become increasingly important. Companies will to start to demand concessions from some of their suppliers, which should stabilize things.

A direct outcome of this sensitivity is that companies have started to place more importance on their discount brands and locations. For example, Metro is more present today in the discount segment. Several Metro supermarkets were converted to the Food Basics banners and most new store openings have been in the discount segment. Companies are also seeing food price deflation, generally a negative development for the industry, which may place additional pressure on retail sales. If food price inflation returns in a meaningful way and consumers remain sticky on prices, companies may be challenged to pass on these added costs to consumers, compressing margins.

Finally, one can argue that competition has never been stronger. Wal-Mart (WMT-N) has done a solid job expanding its fresh produce offerings and continues to lower its prices in Canada. Costco (COST-N) has opened 60+ distribution centres recently, and Amazon (AMZN-N) is testing a new product in the United States where you order online, drive to a central location and pick up your food. Perhaps drones will eventually even drop your groceries off at your doorstep! Regardless, it is important that Canadian retailers keep pace with technology developments/disruptions, and remain focused on building out their online grocery-shopping network as part of an overall digital strategy.

Don't miss our next industry at a glance investment analysis, sign up to the blog below!

Comments

Login to post a comment.